BANDF AD

DRAM and gloom-glut cyclicality

The DRAM bubble is getting bigger with talk of large customers willing to underwrite fab expansion costs to guarantee supply.

Historically the DRAM market has cycled between boom and bust, shortage and over-supply, up-cycle and down-cycle. Some analysts, such as IDC, have been saying this is a supercycle with AI structurally changing the memory market and prolonging the up-cycle because demand will exceed supply out to 2028

There are just three main DRAM suppliers: Micron, Samsung and SK Hynix. It’s an oligopoly and they collectively have pricing control. There are similarities here to the hard disk drive industry where there just three suppliers; Seagate, Toshiba and Western Digital, with a duopoly of Seagate and Western Digital dominant and exerting effective price control by not increasing product capacity with new plants.

BANDF AD

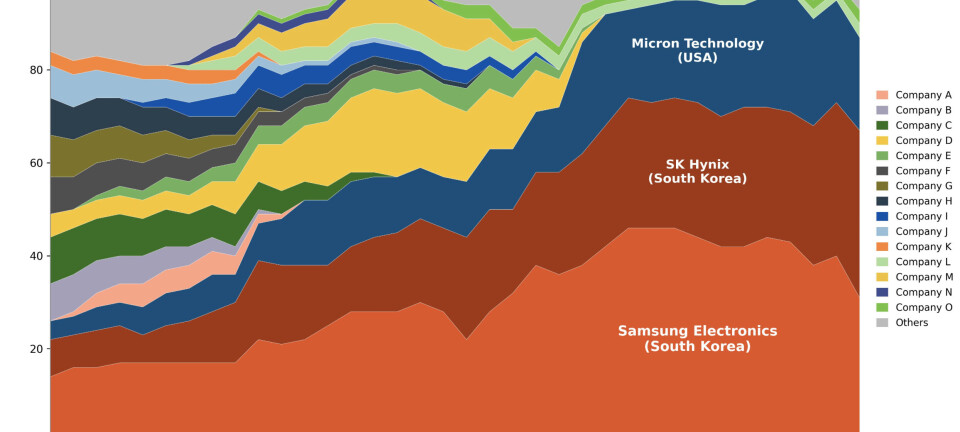

As AI has driven demand for GPU-attached high-bandwidth memory (HBM) to extraordinary and profitable heights, the top three DRAM manufacturers are focusing on this and closing down less profitable consumer and mature, older process DRAM production. A Nomura Asset Management chart shows their dominance.

The current JBM demand strength has been driven by AI training of Large Language Models (LLMS) and it appears likely that the usage of these models in inferencing and AI Agents in reasoning will continue this trend of increased demand.

The top three DRAM fabbers will add hugely expensive DRAM fabrication capacity, but do not want to add too much because, when supply and demand are back in balance, their fabs will still need to churn out DRAM wafers and prices will go down. Their customers don’t see that as the main problem; they want DRAM now.

BANDF AD

A Korean semi-conductor analyst posting as Jukan says SK Hynix has received offers from some major DRAM customers to help fund fab expansion and equipment buying costs. They are proposing dedicated memory production lines with fixed pricing as a way of securing DRAM supply to meet their needs.

Jukan suggests: “This pattern departs from the memory industry's traditional boom-bust cycle, with the industry increasingly viewing the current AI-driven demand growth as long-term structural growth rather than a short-term cycle.”

But is this really signalling the end of the DRAM production boom-bust cycle? Semianalysis commentary thinks not: “In a downturn, the impact of pricing declines can be existential for memory suppliers. By the time pricing rolls over, manufacturers have already committed and deployed multi-billion-dollar capital investments into fabs and equipment that cannot be economically idled. As demand weakens, utilization rates fall, fixed costs are under-absorbed, and cash generation deteriorates rapidly. The result is a sharp compression in gross margins and an inability to earn an adequate return on invested capital precisely when balance-sheet stress is rising.”

We are, Semianalysis says, in an AI inflexion-driven upcycle, and: “such inflection-driven upcycles have not been sustainable in the long run. Prior memory supercycles have tended to peak and roll into downcycles within one or two years, as elevated profitability drives aggressive capital investment, accelerated capacity expansion, and faster-than-anticipated bit supply growth. These supply responses, combined with the inherently cyclical nature of end demand, have consistently led to oversupply and subsequent market corrections.”

BANDF AD

This memory supercycle will eventually peak, possibly in 2028, as prices continue rising until new fab capacity comes on stream. Until then, we can expect Micron, Samsung and SK Hynix, absent natural or other disasters, to be consistently and enormously profitable.