BANDF AD

Spectacular cash generator Sandisk generates spectacular pile of dollars

The acronym SSD could stand for Soaring Sandisk Dollars as it greatly expanded sales into the data center market.

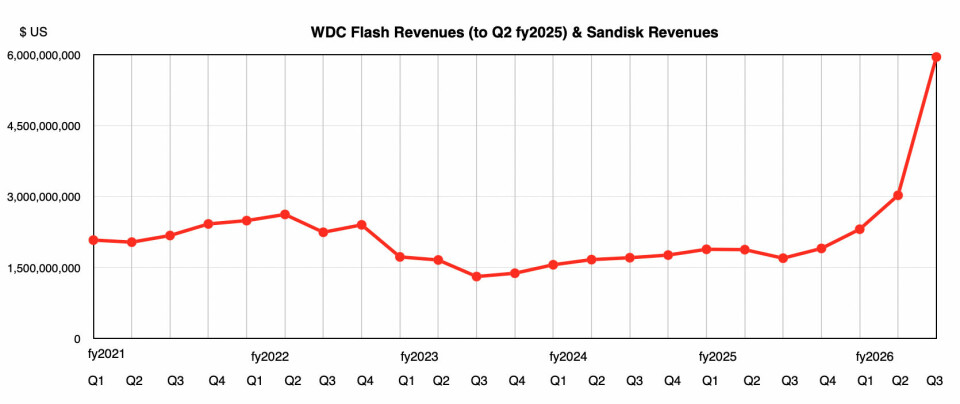

Sandisk resoundingly beat its $4.8 billion high end outlook with third fiscal 2026 quarter, ended April 3, revenues of $5.95 billion, up 251 percent Y/Y, taking advantage of NAND undersupply with higher prices. The GAAP net income number was $3.62 billion, a solid turnaround on the year-ago $1.93 billion loss.

CEO David Goeckeler said: “This quarter marks a fundamental inflection point for Sandisk — where our technology leadership is enabling a deliberate shift in our mix toward the highest-value end markets, led by Datacenter. We are also advancing to a new business model built on multi-year customer engagements backed by firm financial commitments. Together, this transformation is driving structurally higher and more durable earnings power.”

BANDF AD

Sandisk announced a $6 billion share repurchase program and is now debt-free.

Goeckeler added: “With a zero-debt balance sheet, strong cash generation, and a recently authorized share repurchase program, we are positioned to deliver substantial long-term value creation for our shareholders.”

Financial summary

BANDF AD

- Gross margin: 78.4% vs last quarter’s 51.1%

- Operating cash flow: $3.04 billion vs $1.02 billion in prior quarter

- Free cash flow: $2.96 billion vs $843 million in prior quarter

- Cash & cash equivalents: $3.74 billion vs prior quarter’s $1.54 billion

- Diluted EPS: $23.03 vs $5.15 in previous quarter

The three Sandisk market segment revenues were:

- Data center: $1.5 billion, 233% higher Y/Y with more TLC SSD sales

- Edge: $3.7 billion, up 118% with more sales to PCS and smartphones

- Consumer: $820 million, down 10% with a seasonal dip

The company ended the quarter with three signed New Business Model (NBM) agreements, and has already signed two additional NBM agreements in the current quarter. Goeckeler explained the rationale behind the NBMs: “We run a fab. We have very consistent output. We need very consistent consumption. And I think the primary thing — one of the major attributes of these agreements is they give us that.”

BANDF AD

CFO Luis Visoso added:”it's a win-win for us and for our customers. We provide supply, they provide demand, and we have visibility for many years all the way to 5 years.”

There’s another aspect to this, as Goeckeler said: “We're very, very focused on getting the cyclicality out of this business. It's corrosive. It's corrosive to the way we invest our CapEx. It's corrosive to our customers' ability to get a sufficient amount of product to drive their spectacular businesses.”

The three contracts signed during the quarter provide minimum contractual revenue of approximately $42 billion. There are negotiations with several other customers as well. Goeckeler said: “These partnerships are structured to lock in committed supply for our customers and committed financials for Sandisk. Our customers' commitments are backed by firm financial guarantees. These partnerships support durable, structurally higher earnings and a significantly more predictable and less cyclical business for Sandisk.”

Goeckeler belives that AI has changed the NAND market with a: “fundamental shift in underlying infrastructure requirements of artificial intelligence. We are witnessing extraordinary growth, not just in model size, but in resulting token generation, the duration and complexity of model runs and the increasing importance of context. As AI models scale from billions to trillions of parameters and deployments advance from simple inference to deep reasoning and increasingly autonomous agentic systems, NAND has become a critical component of the underlying infrastructure.”

Although demand is higher than supply, Sandisk doesn’t see a need to add new NAND fab capacity, wth Goeckeler saying: “We can continue to drive the bit growth we're talking about mid- to high teens through nodal transitions.” It needs to add more clean-room capacity, “because each node has more steps and more steps is more tools,” but not overall fab capacity. The company has “years of runway into what our nodes are going to be and what the bit growth is going to be from those.”

He views Sandisk as “a spectacular cash generator because the amount of CapEx we need to invest, especially CapEx as a percent of revenue, is continuing to go down substantially.”

Sandisk will start shipping its QLC Stargate SSDs in the current, fiscal fourth, quarter, saying this will add “another layer of revenue growth.”

The fourth quarter outlook is $8 billion +/- $250million, a, wait for it, 320 percent rise on the year-ago quarter’s $1.9 billion. That would enable a $13.95 billion full year revenue number, a 90 per cent uplift on fiscal 2026. Goeckeler said it; Sandisk is a spectacular cash generator.