BANDF AD

Disk drive maker WD beat its own quarterly guidance with AI demand pulling drives off its shelves as fast as it could make them.

Well-run companies making desirable products in a market where customers want more than they can manufacture can make a lot of money, as WD, Seagate, Micron, Samsung, Sandisk and SK Hynix are demonstrating.

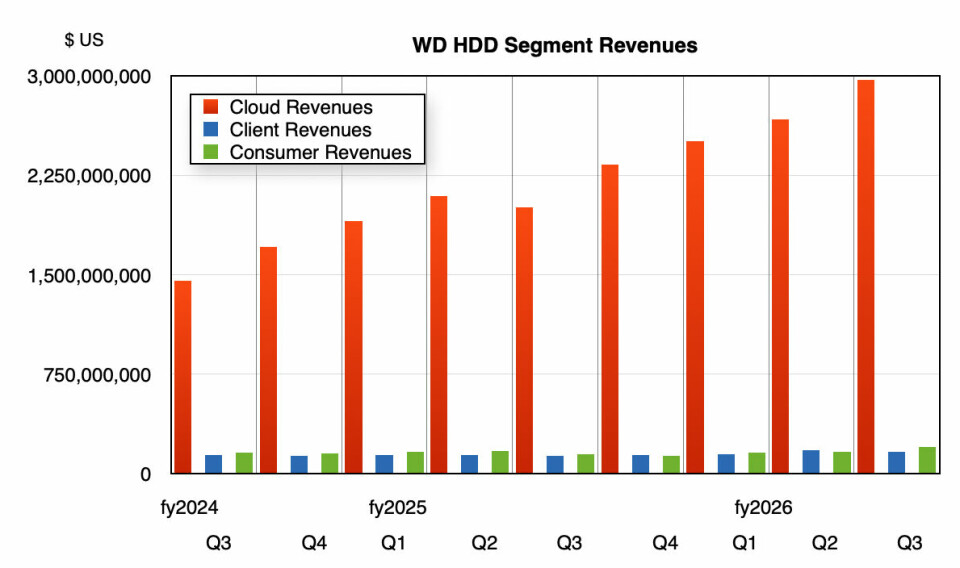

Revenues in WD’s third fiscal 2026 quarter, ended April 3, 2026, were $3.34 billion, 46 per cent more than a year-ago and beating its $3.3 billion outlook. GAAP net income of $3.2 billion, an amazing 96 percent of its revenues, was not what it seemed as it was boosted by a large one-time, non-cash accounting gain related to its retained interest in the spun-off Sandisk (flash memory) business. There was strong demand in all its end markets and an improved pricing environment with more higher-capacity drives sold. Pricing was up 9 percent year over year, although cost per exabyte declined 10 percent.

BANDF AD

CEO Irving Tan said: “WD started calendar year 2026 with great execution, driving strong sequential and year-over-year revenue growth in all our end markets, while expanding gross and operating margins. Gross margin exceeded 50 percent … The demand drivers are clear. Virtually every AI workload, from training, inference, agentic AI to physical AI, creates data that is stored persistently and cost-efficiently on HDDs.”

WD announced a 20 percent increase in the quarterly cash dividend to $0.15 per share. It says it has reduced its debt and achieved a net cash position.

Financial summary:

BANDF AD

- Gross margin: 50.2 percent vs 45.7 percent in prior quarter

- Operating cash flow: $1.12 billion vs $745 million in prior quarter

- Free cash flow: $978 million vs last quarter’s $653 million

- Cash and cash equivalents: $2.05 billion vs prior quarter’s $1.98 billion

- Diluted EPS: $8.20 vs last quarter’s $4.73

The Cloud segment represented 89 percent of WD’s revenues ($3 billion and 48 percent higher Y/Y), with Client at 5 percent ($179 million and up 31 percent annually) and consumer at 6 percent ($186 million and increasing 24 percent Y/Y).

WD shipped 222 EB of capacity: 199 EB of nearline, mass-capacity drives, and 23 EB into other drive sectors; client and consumer mostly. It also said there was increased adoption of its UltraSMR products, Tan saying: “Three of our largest customers have now adopted the technology; two are already meeting nearly all of their exabyte demand with UltraSMR, while the third is rapidly ramping in that direction. We plan to have all of our major customers qualified on UltraSMR by the end of calendar year 2027.”

He added: ”By the end of fiscal year 2027, close to about 60 percent of all the exabytes that we ship will be on UltraSMR.” That will be helped by tier-2 CSP customers buying more if them.

BANDF AD

Its drive IO rate-increasing technologies are being introduced to customers. Tan again: “Our high-bandwidth drives are currently sampling with two hyperscale customers, with an additional customer scheduled to start this quarter. Our dual-pivot technology is being built specifically for new AI workloads.”

A main market trend is the move to increased AI inferencing agentic AI. Tan said in the earnings call: “This larger focus on inference increases the amount of data generated, which in turn increases the need for data storage. … Every token, every prompt, and every query answered and checkpoints saved create data that require persistent, scalable, and cost-efficient storage, and the majority of this data is stored on hard disk drives. As we look ahead, we see the rise of agentic AI, the next wave and arguably the biggest yet.”

In fact: “We expect agentic AI to drive a step-function increase in capacity-oriented storage demand, particularly in cloud and enterprise environments.”

As a result Tan reckons “long-term data storage growth will be greater than 25 percent CAGR.”

In essence there are three HDD demand drivers: AI training, AI inferencing and physical AI. Physical AI refers to robotics, industrial systems, and autonomous vehicle fleets. WD aims to meet these drivers by increasing capacity per drive, through areal density and platter-count increases, rather than by making more drives. Tan said: “Our number one focus is to increase terabytes per disk to make sure we are very competitive within the industry, and beyond that, we can add more platters to the drive as well.”

The demand outlook is getting firmer, with long-term buying agreements with hyperscalers in place reaching out into calendar 2028 and 2029. Tan said: ”We continue to see strong demand from across our client, consumer, and OEM enterprise customers as well.”

That implies that enterprise storage array suppliers, and also SW-defined storage suppliers should all see rising revenues across the next few quarters.

WD’s fourth quarter outlook is for even higher revenues of $3.65 billion +/- $100 million, a 40 percent rise Y/Y at the mid-point. That would make full fy2026 revenues of $12.8 billion, a 34.7 percent increase on fy2025.